Menu

Accessibility settings

Font size:

А

А

А

Color:

Regular version

About Bank

About Bank

Credit Agricole Ukraine

Press centre

Contacts

CSR program «We Care!»

Shareholders

Supervisory Board

Management Board

Directors of commercial sectors

Service Quality

Compliance

Sustainable development strategy

IT Security

Сareer

Partners

Procurement

Pledged property

Notice on the processing of personal data

Information for shareholders and stakeholders

Constituent and other documents, results and company details

IBAN (international bank account number)

Video gallery

Calendar

i-Bank

Online-banking

Online-banking

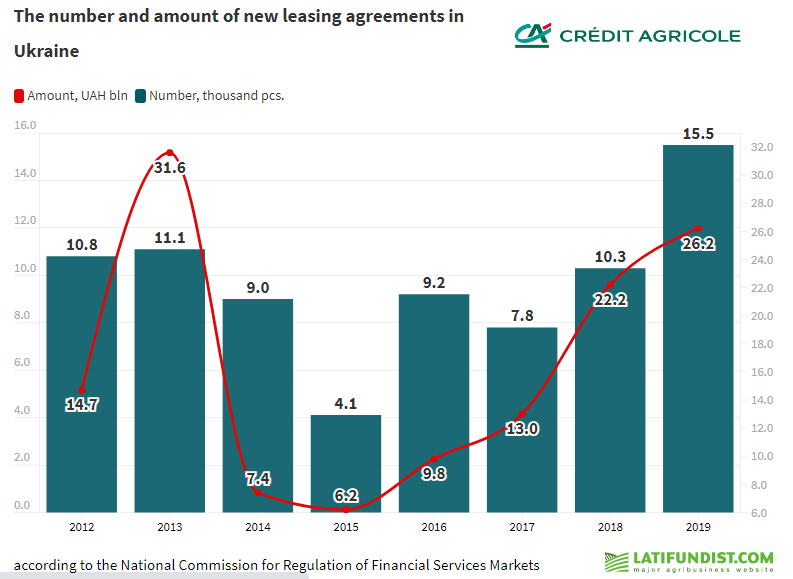

“We observe an upward trend since the leasing market at-large has been growing incrementally from year to year, as well as the demand for leasing services in agricultural sector. Whilst the market has slightly dropped in Q2 due to the coronacrisis, the segment of agricultural leasing continued to grow,” explained

“We observe an upward trend since the leasing market at-large has been growing incrementally from year to year, as well as the demand for leasing services in agricultural sector. Whilst the market has slightly dropped in Q2 due to the coronacrisis, the segment of agricultural leasing continued to grow,” explained “It is good, of course, when a company is consistently profitable. But if it has losses the bank will analyzes in detail each individual case. Besides profit and other basic indicators we analyze a company’s reputation and level of financial management as well. Figures and indicators – that’s good, however, communication with management usually gives much more information,” explained Aleksandre Tchesnakoff.

“It is good, of course, when a company is consistently profitable. But if it has losses the bank will analyzes in detail each individual case. Besides profit and other basic indicators we analyze a company’s reputation and level of financial management as well. Figures and indicators – that’s good, however, communication with management usually gives much more information,” explained Aleksandre Tchesnakoff. According to Aleksandre Tchesnakoff, the biggest advantage of the leasing is the speed of agreement conclusion and receipt of necessary machinery. Indeed, by saving time a businessperson loses less money. It takes Credit Agricole a week or so to make a decision, and then a couple of days more to hand machinery over meaning that the whole process may be finalized within 10 days.

According to Aleksandre Tchesnakoff, the biggest advantage of the leasing is the speed of agreement conclusion and receipt of necessary machinery. Indeed, by saving time a businessperson loses less money. It takes Credit Agricole a week or so to make a decision, and then a couple of days more to hand machinery over meaning that the whole process may be finalized within 10 days.